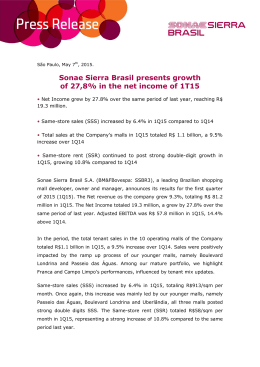

Brazil Retail Overview 2013 - 2014 Brazil Growth The Brazilian retail sector is enjoying the impact of some robust macroeconomic trends. Unemployment remains low and approximately 50 million people have joined the middle class, eager to spend. Sales in shopping centers grew by an annual average of more than 8% in real terms through the last four years, while mature malls continue to exhibit low vacancy rates. This large emerging middle class has a pent-up demand to consume, and new retail developments started to spring up across the country. More than 100 new malls were opened in the last four years, swelling the national total by approximately 27% to 495. Significantly, 50% of these developments are located outside of major metropolitan centers. Second- and third-tier cities, including ones close to the Amazon in the North of the country, have recently gained their own malls. The country is awash with new developments and most cities with at least 250,000 inhabitants have the potential to support a mall-type retail development. This scenario has attracted the interest of international retailers, more than 50 of whom entered the Brazilian market in the last few years. Newcomers range from iconic fastfashion brands Topshop and Forever 21 to luxury retailers such as Tods, Bottega Veneta and Chanel. However, international stores still account for just a small percentage of overall retailing in the country. 2 | Retail Overview 2013 - 2014 Brazil Macro Conditions Macro Figure 2010 2011 2012 2013 2014 (E) 2015 (E) GDP Growth Rate (%) 7.5 2.7 1.0 2.3 1.8 2.7 Inflation (%) 5.9 6.5 5.8 5.9 6.0 5.7 Unemployment Rate (%) 6.7 6.0 5.5 5.4 5.8 6.0 SELIC Interest Rate (%) 10.66 10.9 7.14 9.9 11.33 12.11 Mall Sales Growth yoy (%) 14.2 13.3 15.5 8 6-8 5-7 IMF, Brazil Central Bank, IBGE, OIT, JLL Analysis • Total Land Area: 8,515,767 km² (the 5th largest in the World); • 5th largest population (2,8% of the world population); • 6th GDP in the world and first in Latin America (2.7 USD Tr - IMF 2013); • The middle-class increased and today represents half of total brazilian population. GLA distribution by region North 5% 560,407 sqm 21 Malls Northeast 15% 1,959,751 sqm 68 Malls Mid-West 8% 1,069,906 sqm 45 Malls Southeast 58% 7,537,708 sqm 247 Malls GLA Total Stock 12,9 M sqm South 14% 1,812,606 sqm 87 Malls Retail Summary • Total Shopping Centers 2013: 495 • GLA Stock 2013 (millions sqm): 12.940 • To be opened in 2014: 39 Malls (1,113,304 sqm) • To be opened in 2015: 19 Malls (514,185 sqm) • Density: 64 sqm/1,000 inhabitants • Sales in Shopping Centers increased 8,4% from 2012 • 2013 sales: R$ 129 billion • Average traffic: 415 million visitors/ month • Mall average size: 25,500 sqm • Generated jobs: 843,254 Abrasce, JLL Analysis (April 2014) Retail Overview 2013 - 2014 | 3 Mall Market Evolution 363 351 43.5 45.3 46.7 7.492 8.253 8.645 9.081 2006 2007 2008 2009 39.9 408 392 376 48.5 9.512 2010 GLA (Millions sqm) 430 52.2 10.344 2011 457 57.0 11.403 2012 # Malls 495 64.1 12.94 2013 535 69.5 14.106 2014 (E) 558 72.4 14.803 2015 (E) GLA/1k Inhabitants The numbers demonstrate nominal growth since 2009 in all fronts: 26% in new developments; 42% in GLA and 74% in total sales. These indicators show the consumption in Brazilian malls is growing, despite the high interest rate making the sale’s national average of approximate R$12.000/square meter. Malls Total Sale 160 140 140 120 129 119 100 80 91 74 60 40 108 CAGR 13.7% (BRL) 14% (USD) 58 23.9 31.5 68.8 69.0 68.3 2012 2013 2014 (E) 58.7 50 20 73.5 64,6 38.2 41.1 2008 2009 0 2006 2007 2010 2011 USD (Billion/yr) BRL (Billion/yr) Malls GLA (sqm) Sales (R$ billion, nominal) 4 | Retail Overview 2013 - 2014 2009 2013 Growth 392 495 26% 9.081 12.94 42% 74 129 74% Property Size (GLA) Mix (GLA) Super Regional 8% Regional 19% Food 18% Small 29% Fashion 45% Others 13% Home Goods 5% Medium 44% Convenience/Services 13% Small: up to 20 thousand sqm Medium: from 20-40 thousand sqm Regional: from 40-60 thousand sqm Super Regional: over 60 thousand sqm Leisure/ Entertainment 2% Personal Care 4% Increased integration to the international market New entrants by year Up to 2012 Tiffany (2001) Mac (2002) D&G (2004) Gucci (2008) Chanel (2010) Burberry (2010) Hooters (2010) Prada (2011) Bottega Veneta (2011) Kate Spade (2011) 2012 Balmain Vapiano Coach Sephora Top Shop MiuMiu Lanvin Goyard Tory Burch Paula Cahen D’Anves Officine Panerai Van Cleef & Arpels Etiqueta Negra Zara Home Balenciaga IWC Jaeger LeCoultre Vans Laudurée 2013 Breitling Guess Fendi Repetto Fred Perry Armani Home Holly Hunt Cruciani Johnie Walker Store Cremeria Vienna Le Bilboquet Nicole Miller TOD’s Cold Stone Desigual Rochas Europea Gourmet New Balance Michael Kors Anne Fontaine Yellow Veuvet Clicquot 1Q2014 Johnny Rockets Gelateria Dri Dri Tony Roma’s Forever 21 Vitra Apple Chosen City for the 1st Store Rio de Janeiro: 7% Others: 5% São Paulo: 88% Retail Overview 2013 - 2014 | 5 Global retail investment landscape A diversity of investment opportunities Investment Activity High Long-Term Development Cycle Medium Italy Brazil Spain Russia Poland UK Turkey Taiwan Germany Mexico Czech Rep Hong Kong Long-Term Investment Cycle Main Characteristics of a Growth Market: Romania Hungary Japan Venezuela Ukraine Thailand France Nigeria Indonesia Malaysia Nordics Colombia Vietnam South Korea Netherlands Bangladesh Peru Argentina Portugal Singapore Pakistan Morocco Chile Greece Belgium US Bangladesh Egypt India UAE Switzerland Australia Pakistan Kazakhstan Saudi Arabia South Africa Austria Canada Frontier Emerging Growth Transitional Mature Advanced Algeria Low China After the surge in new malls, a wave of acquisitions and consolidation is likely to follow: *This is a general representation of each country’s current position on the evolution curve as it relates to major malls based on direct investment volumes, construction activity, transparency and international retailer activity. • Mainly development; • Increasing investor interest; • Limited liquidity; • Semi-transparent (negotiation); • Strong stock growth 10-20% pa; • International Retailers: Primary target; • Expansion into tier 2 and 3 cities. • Franchises dominate, but some buy-backs. Brazil Main Retail Transactions 2013 In 2013, most of Brazil Capital Markets activity in Shopping malls came from local companies, such as Iguatemi and Aliansce, acting as integrators and increasing their equity stake in shopping malls they already operate. Cap rates have increased, following the upward trend in the SELIC rate, which is now at 11%. Most interest is in operating malls, and we have seen a cooling in project acquisition appetite. Also notable is the return of Westfield’s 50% stake in Brazilian JV with Almeida Junior back to Almeida Junior, for book value. Official reports cite the difference in long term perspectives as reasons for the return. In February 2014, Iguatemi and TIAA-CREF announced the acquisition of WTorre´s 50% stake in JK Iguatemi, one of the most prestigious Shopping Centers in Brazil. R$636 MM were paid for for 50% of the total GLA of 36,000 sqm, plus a future earnout to WTorre. 6 | Retail Overview 2013 - 2014 Quarter City/State Property Name Vendor Purchaser Area Sale price Acquired (R$ MM) (sqm) Q1 Campinas (SP) Prado Shopping Center Unknown Gazit-Globe 9.500 40,00 Q1 Sorocaba (SP) Shopping Iguatemi Esplanada IESC - Iguatemi Previ 13.789 13,60 Q2 Fortaleza (CE) Shopping Parangaba Unknown Aliansce 12.749 118,00 Q3 Bauru (SP) Boulevard Shopping Nações Bauru Carlyle Group Aliansce 5.700 34,50 Q3 Rio de Janeiro (RJ) Via Parque Shopping Unknown Aliansce 1.774 11,50 Q3 Novo Hamburgo (RS) Shopping Platinum Outlet São José Des. Imob. IESC - Iguatemi 8.236 46,20 Q3 Franca (SP) Terreno para Expansão Franca Shopping Unknown Sonae Sierra 24,00 Q4 Campinas (SP) Shopping Galleria Luis Roberto C. Nogueira IESC - Iguatemi 9.971 Q4 São Paulo (SP) Shopping Pátio Higienópolis Fundação Conrado Wessel JHSF 6.302 350,00 Q4 Bauru (SP) Boulevard Shopping Nações Bauru Grupo Vértico Aliansce 2.600 23,00 Q4 Campinas (SP) Shopping Galleria Anhumas IESC - Iguatem 6.647 55,74 122.733 800 45.466 Total 83,60 Real Capital Analytics, JLL Repurchase of Almeida Junior from Westfield Quarter City/State Property Name Vendor Purchaser Area Sale price Acquired (R$ MM) (sqm) Q2 Blumenau (SC) Blumenau Norte Shopping Westfield Group Almeida Junior 57.372 190,33 Q2 Blumenau (SC) Shopping Center Neumarket Blumenau Westfield Group Almeida Junior 15.750 167,61 Q2 Camboriu (SC) Balneario Camboriu Shopping Westfield Group Almeida Junior 12.500 136,83 Q2 Joinville (SC) Joinville Garten Shopping Westfield Group Almeida Junior 15.000 187,175 Q2 São José (SC) Continente Park Shopping Westfield Group Almeida Junior 21.000 240,765 121.621 923 Total Real Capital Analytics, JLL Iguatemi will end up with 64% of the JK Iguatemi and TIAA-CREF with 36%. This transaction, still under due diligence, hints the scope of future transactions in this sector: Focus on prime assets in consolidated markets, with growing tickets and with institutional investors. Rental Prices are coolling off and decreasing in secondary markets Prime Retail - Rental Clock, Q4 2013 São Paulo, Rio de Janeiro Berlin, Paris, Hong Kong Brazil: Tier 2 and 3 cities Moscow Rental Value growth slowing Beijing London Rental Values falling Americas EMEA Asia Pacific Rental Value growth accelerating London Rental Values bottoming out Dubai, Mumbai, San Francisco Miami, New York, Huston, Delhi Chicago Madrid Singapore Washington DC Boston, Los Angeles,Shanghai Milan, Sydney US positions relate to the overall market Source: Jones Lang LaSalle, January 2014 Retail Assets are more resistant than office and industrial 20% 18% 16% 14% 12% 10% 8% 6% 2005 2006 2007 H1 2008 H2 2008 Industrial & Logistic H1 2009 H2 2009 H1 2010 Retail H2 2010 H1 2011 H2 2011 H1 2012 Office H2 2012 H1 2013 H2 H1 H2 2013 2014 F* 2014 F* Interest Rate (SELIC) Retail Overview 2013 - 2014 | 7 The future The retail sector in Brazil has had a tremendous growth in the past years and the vast majority of developers today understand its value. Most new urban office tower and hotel have a retail component. There are several mixed-use projects being completed and the few already in place are enjoying great results. The urban enclosed malls represent the majority of existing developments; however we started to notice some other formats being developed such as Outlets, Power Centers, Strip Centers and Life Style Centers. In terms of structure, the future of the sector is likely to undergo consolidation in secondary markets and increase in efficiency and liquidity (some with international money) in the prime markets. International retailers shall continue to debut in Brazil despite the entrance barriers still in place. This is bringing more competition to the local retailers though helping to raise the bar for the market in general. We envision the continue professionalization and maturing of the market stakeholders. Finally, we noticed the foreign companies that do best in Brazil are the ones who make a long term commitment to be in Brazil, avoiding basing its decision on the humor of the economy at a given moment. Brazil has had good improvements in the last decade, but still has a lot more to go. The economy might have its ups and downs in the process of greatness, so the enterprises that are here regardless of the speed bumps, shall have greater chance of reaping the benefits of this great market of 200 million people. São Paulo Av. Das Nações Unidas, 12.551, 23rd floor 04578-903 São Paulo/SP Tel: +55 11 3043-6900 Fax: +55 11 -3043-6999 Monica Lee Global Clients Leader Phone: + 55 11 3043-6947 Mobile: + 55 11 97544-5208 [email protected] Rio de Janeiro Av. Presidente Wilson, 113, 10th floor 20030-020 Rio de Janeiro/RJ Tel: +55 21 2277-2700 Fax: +55 21 2277-2749 Márcia Castro Retail Division Leader Phone: + 55 11 3043-6893 Mobile: + 55 11 96393-3129 [email protected] JLL Brasil www.jll.com.br facebook.com/JonesLangLaSalleBrasil Twitter: @jllbrasil linkedin.com/company/jll Team Global Clients Marco Lacayo Phone: + 55 11 3043-8565 Rafael Calvo Phone: + 55 11 3043-6257 Marina Lima Phone: + 55 11 3043-6972 Team Client Solutions José Cardim Phone (SP): + 55 11 3043-7183 Paulo Casoni Phone (SP): + 55 11 3043-6935 Marcelo Sasaki Phone (SP): + 55 11 3043-6897 Roberto Patiño Phone (SP): + 55 11 3043-7140 For more information, please contact: www.jll.com.br/brazil/en-us

Baixar