☰

Explorar

Assinar em

Inscrever-se

Envio

×

Baixar

Sem categoria

ferreira josé

The Caixa Economica: A Social and Economic History of

Author(s) Fernanda Santos Freitas , Cristiane Carneiro Thompson

Maria José Coracini Unicamp – IEL/DLA

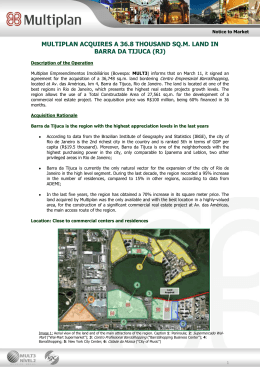

multiplan acquires a 36.8 thousand sq.m. land in barra da tijuca (rj)

AULÃO PRÉ-UNIVERSITÁRIO

ChromaPipe: a pipeline for analysis, quality control - Funpec-RP

Inclusion of the Call Notice and Management Proposal

Rio de Janeiro: in a [Brazil] nutshell

Pathological Implications of Nucleic Acids Interactions - SIG

CURATORIAL RESIDENCY PROGRAMME [ BIOS ]

![Rio de Janeiro: in a [Brazil] nutshell](http://s1.livrozilla.com/store/data/000267057_1-8f3d383ec71e8e33a02494044d20674d-260x520.png)

![CURATORIAL RESIDENCY PROGRAMME [ BIOS ]](http://s1.livrozilla.com/store/data/000349088_1-1b4ebb77fda70e90436648914a2832a0-260x520.png)